Introduction: The Unthinkable Scenario

For generations, the S&P 500 has been the bedrock of long-term wealth creation. The prevailing wisdom has been simple: invest in a low-cost index fund, hold on through the inevitable ups and downs, and let the power of compounding work its magic. This strategy, championed by icons like Warren Buffett, has proven remarkably effective for most of the last century. However, what happens when this foundational principle is put to its most severe test? What if, instead of a typical bear market that recovers in a few years, investors face a prolonged period of stagnation—a “lost decade”—where the index delivers zero or negative real returns over ten years or more? Understanding how to survive a lost decade for the S&P 500 stock market outlook is not about fear-mongering; it is about prudent preparation. It requires shifting from a mindset of passive accumulation to one of active resilience, ensuring that a temporary period of market stagnation does not derail a lifetime of financial goals.

The concept of a lost decade is not a hypothetical doomsday scenario. It has happened before. For investors who entered the market in 2000, at the peak of the dot-com bubble, the S&P 500 did not regain its previous high until 2007, only to be immediately battered by the Global Financial Crisis. By March 2009, the index was down over 50% from its 2000 peak. For those ten years, the nominal return was negative. When adjusted for inflation, the loss was even more profound. The period from 1968 to 1982 was another stark example, where the market moved sideways for over a decade as it grappled with high inflation and economic stagnation. These historical precedents serve as powerful reminders that while the market’s long-term trajectory is upward, the journey can be punctuated by long, challenging plateaus.

This article is designed to serve as a strategic guide for navigating such a period. We will explore not only the historical context of market stagnation but also the psychological fortitude required to withstand it. More importantly, we will delve into practical, actionable strategies—from diversification and income generation to tactical asset allocation and the power of continuous investment. The goal is to provide a roadmap that allows you to protect your capital, maintain your standard of living, and even position yourself for significant growth when the market eventually resumes its upward climb.

Understanding the Lost Decade Phenomenon

What Defines a Lost Decade for the Stock Market?

In financial terms, a “lost decade” refers to a prolonged period where the primary stock market index, such as the S&P 500, delivers a cumulative return that is flat or negative after accounting for inflation. It’s not necessarily a decade of unrelenting decline; rather, it’s characterized by high volatility, sharp bear markets, and subsequent recoveries that merely bring the index back to its starting point. This creates a “whipsaw” effect that can be devastating for investors who are not prepared.

The mechanics behind such a period are complex. They often involve a confluence of factors: a severe overvaluation of stocks (like the Nifty Fifty in the 1970s or the dot-com bubble in the 2000s), followed by a painful revaluation; persistent macroeconomic challenges such as stagflation or a debt crisis; and a shifting of capital from equities to other asset classes like bonds, real estate, or commodities. For the average investor, a lost decade is less about the absolute loss of capital (though that can happen) and more about the opportunity cost—the years of lost compounding that can significantly impact retirement readiness.

A Look Back: 2000-2010

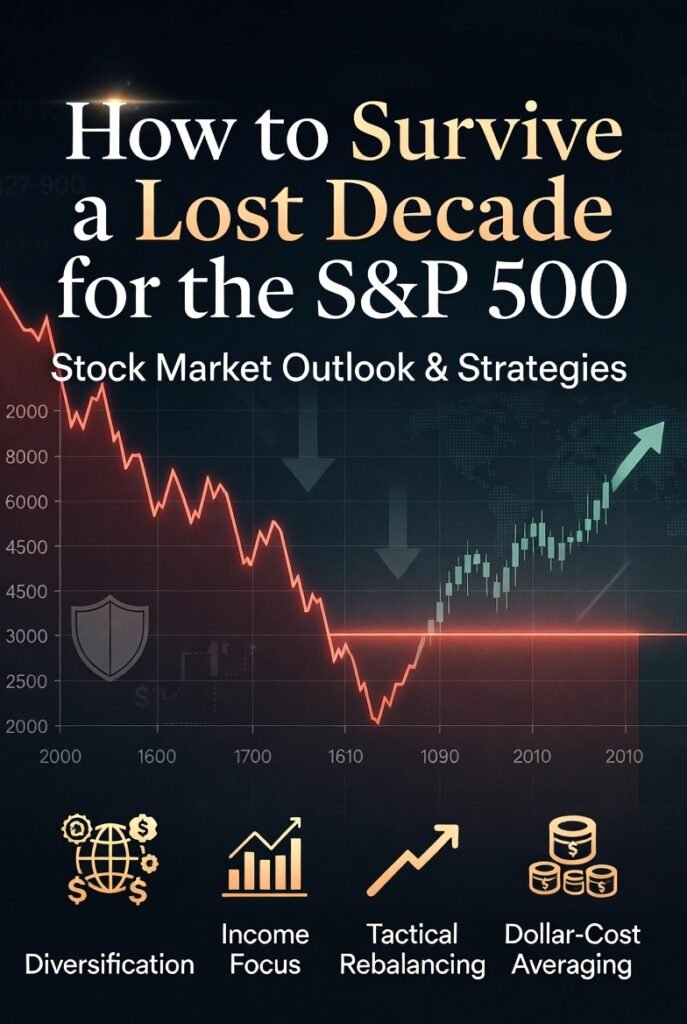

The most recent and vivid example for today’s investors is the period from 2000 to 2010. This decade was bookended by two of the most significant bear markets since the Great Depression. The collapse of the dot-com bubble saw the S&P 500 fall by nearly 50% from its peak in March 2000 to its trough in October 2002. A recovery followed, but it was short-lived. By 2007, the index had just surpassed its previous high, only to be plunged into a new crisis. The Global Financial Crisis, triggered by the collapse of the housing bubble and the subsequent banking crisis, sent the S&P 500 plummeting by another 57% from its 2007 peak to its low in March 2009. By the end of the decade, the S&P 500 had lost approximately 10% of its value on a nominal basis. An investor who had put $100,000 into the S&P 500 at the start of 2000 would have had roughly $90,000 by the end of 2010, a devastating result for anyone planning to retire during that period.

The lessons from this decade are crucial. It taught investors that buy-and-hold, while a sound long-term strategy, is not a strategy that can be mindlessly applied without consideration for valuation and portfolio structure. It highlighted the importance of risk management and the dangers of concentration in a single asset class.

The Psychological Toll

Surviving a lost decade is as much a psychological challenge as it is a financial one. The human mind is wired to extrapolate recent events into the future. After several years of market declines or stagnation, it becomes incredibly difficult to maintain the conviction to stay invested. The constant negative news cycle, coupled with the visible erosion of portfolio value, leads to what behavioral economists call “loss aversion”—the tendency for people to feel the pain of a loss more acutely than the pleasure of a gain.

This psychological pressure often forces investors to make the worst possible decision: selling at the bottom. When an investor capitulates during a prolonged downturn, they lock in their losses and miss out on the subsequent recovery. A lost decade tests patience and discipline to their absolute limits. It requires a stoic mindset, a focus on long-term data over short-term emotion, and a clearly defined plan that is adhered to when fear is at its peak.

Key Strategies for Navigating Market Stagnation

Strategy 1: Redefine Diversification

In a traditional bull market, a simple 60/40 portfolio (60% stocks, 40% bonds) often suffices. However, in a lost decade scenario, this portfolio can be insufficient, especially if bonds also face headwinds from rising interest rates. True diversification for survival requires looking beyond the traditional asset classes.

Investors should consider expanding their portfolio to include a broader range of uncorrelated assets. Real assets like real estate or inflation-protected securities (TIPS) can provide a hedge against inflation, which was a major feature of the 1970s lost decade. Commodities, such as precious metals, can also act as a store of value when paper assets are under pressure. For instance, during the 2000-2010 lost decade, gold was one of the best-performing assets, rising from around $280 per ounce to over $1,400.

Another crucial element is global diversification. A lost decade can be specific to the U.S. market. While the S&P 500 stagnated in the 2000s, emerging markets like China and Brazil, as well as commodity-producing nations like Canada and Australia, delivered strong returns. By allocating a portion of a portfolio to international markets, an investor can tap into growth engines outside of the one experiencing stagnation. For those looking to understand how to structure such a globally resilient portfolio, resources on market analysis and growth strategies can be invaluable. A deep understanding of different economic cycles can help identify which regions and sectors are poised for growth while others falter.

Strategy 2: Focus on Income and Cash Flow

When capital appreciation is scarce, income becomes the primary driver of total return. In a lost decade, a dollar of dividend income is worth significantly more than a dollar of unrealized capital gain, because that income can be reinvested to buy more shares at depressed prices, setting the stage for outsized gains when the market eventually recovers.

Building a portfolio focused on high-quality, dividend-paying stocks is a cornerstone of this strategy. Look for companies with a long history of not only paying but increasing their dividends—often called “Dividend Aristocrats.” These are typically established, cash-rich companies in sectors like consumer staples, healthcare, and utilities. Their products are in demand regardless of the economic climate, providing a level of earnings stability that supports their dividend payments.

Beyond equities, fixed-income investments like bonds and certificates of deposit (CDs) can provide a steady, predictable income stream. In a rising interest rate environment, which can often accompany a lost decade, new bonds issued with higher yields become increasingly attractive. The key is to build a laddered bond portfolio, where bonds mature at staggered intervals, allowing the investor to continuously reinvest principal at the prevailing higher rates. This income-focused approach transforms a portfolio from a speculative asset to a cash-flow generating asset, providing both financial stability and the psychological comfort of a regular paycheck from your investments.

Strategy 3: Embrace Tactical Asset Allocation and Rebalancing

During a prolonged period of high volatility, a passive, set-it-and-forget-it strategy is not enough. Investors need to become more active in their portfolio management, specifically through the discipline of rebalancing. Rebalancing is the process of periodically selling assets that have performed well and buying assets that have underperformed to return the portfolio to its target allocation.

In a lost decade characterized by violent swings, this discipline can be a powerful source of returns. For example, during the 2000-2002 bear market, a disciplined rebalancer would have been selling bonds and other non-equity assets that held their value to buy stocks at deeply discounted prices. Then, as stocks rebounded from 2003 to 2007, they would have been selling those appreciated stocks to buy bonds and other assets that had become relatively cheaper. This systematic approach of “buying low and selling high” can allow an investor to generate positive returns even in a flat overall market.

Tactical asset allocation takes this a step further. It involves making strategic shifts in the portfolio based on long-term valuations and macroeconomic trends. For instance, an investor might reduce their allocation to U.S. large-cap stocks when the Shiller P/E ratio (a measure of long-term valuation) is at historically high levels and increase their allocation to value stocks, international markets, or alternative assets. This does not mean trying to time the market on a daily or weekly basis, but rather making informed, gradual adjustments based on a clear understanding of market cycles.

Strategy 4: The Power of Continuous Investment (Dollar-Cost Averaging)

Perhaps the single most powerful tool for an individual investor to survive—and even thrive—during a lost decade is dollar-cost averaging (DCA) . DCA is the practice of investing a fixed amount of money at regular intervals, regardless of the share price. This strategy is the antithesis of the emotional decision-making that leads to buying high and selling low.

When the market is in a prolonged decline or stagnation, DCA allows an investor to accumulate shares at a lower average cost. Each investment buys more shares when prices are low and fewer when prices are high. Over time, this can dramatically lower the portfolio’s cost basis.

Consider the investor who started in 2000. If they had simply made a lump-sum investment and stopped, they would have ended the decade with a loss. However, if they had continued to invest a fixed amount every month throughout the entire decade, they would have been buying shares at the lowest prices of 2002 and 2009. By the end of 2010, the investor using DCA would have not only recouped their losses but would have likely seen significant gains. This is because they were able to accumulate a large number of shares at the market’s lowest points, positioning them for the powerful bull market that followed from 2010 onward. This strategy transforms a lost decade from a period of destruction into a period of accumulation.

Protecting Your Retirement in a Stagnant Market

Revisiting the 4% Rule

For retirees and those nearing retirement, a lost decade represents an existential threat. The widely cited “4% rule”—which suggests retirees can withdraw 4% of their portfolio in the first year of retirement and adjust for inflation thereafter—was developed using historical market data that included periods of strong returns. It was not designed to withstand a lost decade that occurs in the first ten years of retirement, a phenomenon known as “sequence of returns risk.”

Sequence of returns risk is the danger of experiencing poor investment returns early in retirement. If a retiree is forced to sell assets to fund their living expenses during a prolonged bear market or stagnation, they deplete their portfolio at an accelerated rate, leaving less capital to participate in the subsequent recovery. This can lead to portfolio failure much earlier than projected.

To mitigate this risk, retirees need a more flexible and robust withdrawal strategy. This might involve:

- Reducing withdrawals during years of negative returns to preserve capital.

- Building a “cash buffer” of 2-3 years of living expenses in low-risk, liquid assets (like a high-yield savings account or short-term Treasury bills). This buffer allows the retiree to cover expenses without being forced to sell equities during a market downturn, giving the portfolio time to recover.

- Annuities: A portion of the portfolio can be allocated to a single premium immediate annuity (SPIA) to create a guaranteed income stream that covers essential living expenses. This provides a financial foundation, allowing the rest of the portfolio to be invested for long-term growth without the pressure of needing to generate income for basic needs.

The Importance of Financial Planning and Professional Guidance

Navigating a lost decade is not a solo endeavor. The complexity of managing sequence of returns risk, tax implications of rebalancing, and the psychological pressure to make impulsive decisions make this an ideal time to seek professional guidance. A fee-only financial advisor can act as a behavioral coach, helping the investor stay disciplined and focused on the long-term plan. They can also provide sophisticated financial planning that goes beyond investment management, incorporating tax-loss harvesting strategies to offset capital gains, and optimizing withdrawal strategies from different account types (taxable, tax-deferred, and tax-free) to maximize after-tax income.

To further understand the business environment and market dynamics discussed here, readers can explore related topics. For insights into how global shifts influence corporate strategy and market positioning, you can read about essential business fundamentals in our article on What Is Business?. Additionally, understanding the landscape of financial opportunities requires a grasp of modern trading environments, which you can explore in our piece on Financial Markets. For those interested in how geopolitical stability affects emerging sectors, our analysis on Digital Economy Trends provides valuable context on how non-traditional assets respond to macroeconomic pressures.

Conclusion: A Mindset for Resilience

The prospect of a lost decade for the S&P 500 is daunting, but it does not have to be a financial catastrophe. The difference between surviving and thriving in such an environment lies in preparation and mindset. By understanding that the core challenge is how to survive a lost decade for the S&P 500 stock market outlook, an investor can move from a state of passive anxiety to one of active, strategic control.

The strategies outlined here—from expanding your definition of diversification and focusing on income to embracing tactical rebalancing and the power of disciplined, continuous investment—are not merely defensive maneuvers. They represent a holistic approach to wealth management that builds resilience. By preparing for the worst-case scenario, you equip yourself to handle all market conditions with confidence. History shows that while markets can stagnate for long periods, they do not do so forever. The lost decades of the 1930s, 1970s, and 2000s were each followed by powerful, multi-year bull markets that rewarded those who maintained their discipline and their capital.

Ultimately, the goal is to ensure that your financial life is not dictated by the whims of the stock market. By building a robust portfolio designed to generate income and preserve capital through diversification and a long-term perspective, you can achieve financial independence regardless of what the market does over the next ten years. The journey may be challenging, but with a sound plan, steadfast discipline, and a focus on what you can control, you can not only survive a lost decade but emerge from it in a position of strength.