")

The narrative of young adulthood has always been one of struggle—a period of navigating first jobs, building credit, and learning the ropes of financial independence. However, the year 2026 presents a starkly different reality. What was once a temporary phase of “being broke” has, for an alarming number of individuals under 35, transformed into a formal, life-altering declaration of insolvency. The reasons more young people are filing for bankruptcy in 2026 are not merely a continuation of past trends but represent a convergence of new economic structures, societal shifts, and systemic pressures that previous generations did not face at the same scale.

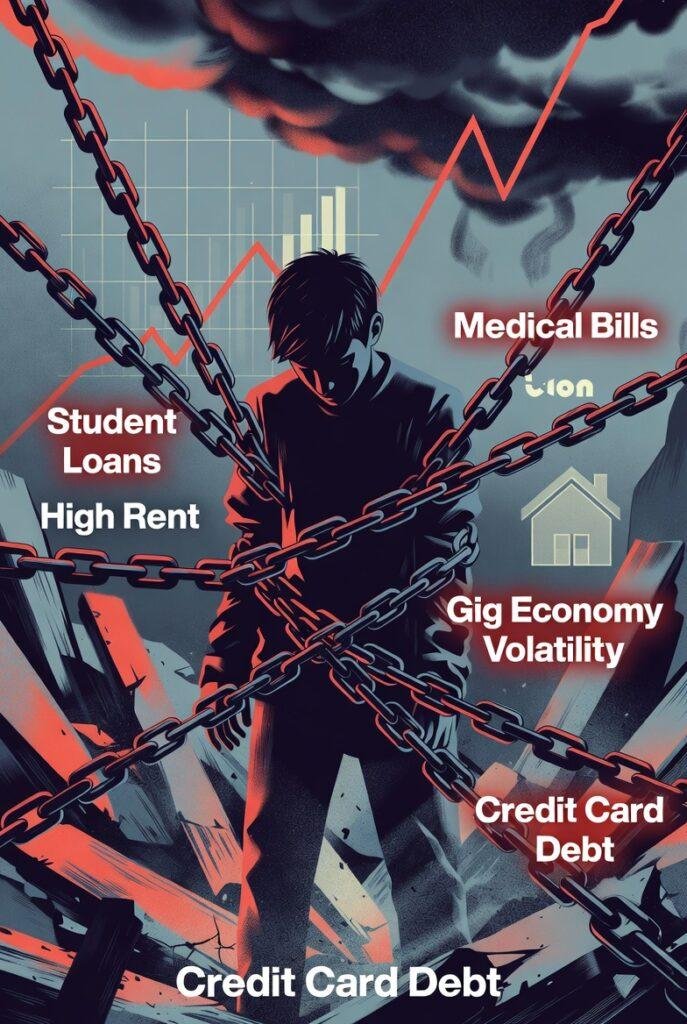

Bankruptcy, once considered a financial last resort associated with older generations facing business failure or medical catastrophe, is now becoming a grim milestone for the young. This is not a story of individual irresponsibility; rather, it is a reflection of a complex web where stagnant wage growth meets soaring living costs, where the very tools designed to create opportunity (like student loans and credit cards) have become shackles, and where a volatile global economy leaves those with the least financial cushion most vulnerable.

The Shifting Economic Landscape for Young Adults

To understand this phenomenon, we must first examine the economic terrain that young people are navigating. The years following the global pandemic ushered in an era of “polycrisis”—a term economists use to describe multiple, interconnected shocks occurring simultaneously. For those entering the workforce between 2020 and 2026, this has meant starting their careers in an environment of uncertainty.

Stagnant Wages Versus Inflationary Pressures

While official inflation rates have stabilized compared to the peaks of earlier years, the cumulative effect of sustained price increases on essentials—housing, food, transportation—has permanently altered the cost of living. Entry-level wages, even in professional sectors, have not kept pace with this cumulative inflation. A young professional today may earn nominally more than their counterpart in 2020, but their real purchasing power is significantly diminished. This disconnect is a foundational reason more young people are filing for bankruptcy in 2026, as even a minor financial disruption can shatter a budget that leaves no room for error.

The Gig Economy and Income Volatility

The traditional model of a stable, long-term job with predictable income and benefits has eroded. Many young adults cobble together income from multiple gig economy roles. While this offers flexibility, it introduces extreme income volatility and lacks the safety nets of employer-sponsored health insurance, retirement contributions, or paid leave. One week of illness, a car breakdown, or a platform’s algorithm change can result in a sudden 40% drop in income. For those without family wealth to fall back on, this volatility turns manageable debt into a crisis.

The Heavy Burden of Educational Debt

Perhaps no single factor is as synonymous with the millennial and Gen Z financial experience as the weight of student loans. Unlike previous generations where higher education was a more attainable investment, the cost of tuition has ballooned over the past two decades, creating a debt load that many find insurmountable.

The Repayment Restart Shock

For many young people, the early 2020s offered a temporary reprieve from federal student loan payments due to pandemic-era pauses. When repayment restarted with full force, it introduced a “payment shock” for millions who had structured their finances around its absence. For those who had defaulted on other obligations to stay afloat during the pause, the resumption forced an impossible choice: pay the student loan or pay for housing and food. Bankruptcy law, notoriously difficult for discharging student loans, provides little relief, but the weight of this debt often forces individuals into bankruptcy to manage the other debts that accumulated while trying to pay educational loans.

The Value Proposition Debate

Compounding the problem is a growing skepticism about the return on investment for higher education. Many young people took on six-figure debt based on promises of stable, high-paying careers. However, market saturation in fields like law, certain branches of technology, and creative industries has meant that starting salaries have not risen commensurately with debt loads. This mismatch between investment and outcome leaves a generation feeling trapped, with a monthly debt obligation that rivals a mortgage but for an asset that does not generate proportional income.

Healthcare: The Unpredictable Financial Catastrophe

Despite ongoing policy debates, the United States remains a nation where a single health crisis can lead to financial ruin. For young people, who are often in the “coverage gap”—too old to be on a parent’s plan but without access to employer-sponsored insurance—the risk is acute.

High-Deductible Plans and Underinsurance

Many young adults, even those with insurance, are enrolled in high-deductible health plans that keep monthly premiums low but expose them to thousands of dollars in out-of-pocket costs before coverage truly kicks in. An unexpected appendicitis, a car accident, or a mental health crisis requiring hospitalization can result in a $5,000 to $10,000 bill overnight. For someone living paycheck to paycheck, this is not merely a debt; it is a debt that often leads to credit card borrowing, which then spirals. Medical debt remains one of the primary drivers of bankruptcy filings across all age groups, and its impact on the young is magnified because they lack the accumulated assets to absorb the shock.

Mental Health Costs

The ongoing mental health crisis among young adults adds another layer. Access to consistent therapy, psychiatric care, and medication is expensive. Many forgo care due to cost, but those who seek it often incur significant debt. The cycle is cruel: financial stress exacerbates mental health struggles, which in turn can lead to job loss or reduced earning capacity, further deepening the financial hole.

The Housing Crisis and the Rent Trap

Homeownership, once a primary mechanism for wealth building, has become an unattainable dream for a significant portion of the young population. The 2026 housing market is characterized by persistently high prices and elevated interest rates, pricing out first-time buyers and leaving them in a precarious rental market.

Rent as a Financial Anchor

Rents have increased at rates far exceeding wage growth in most metropolitan areas. The common financial rule suggests spending no more than 30% of gross income on housing. For many young adults, that figure now exceeds 50%. This “rent burden” leaves less for savings, debt repayment, and emergency funds. When a financial shock occurs—a car repair, a medical bill—there is no buffer. The result is a reliance on high-interest credit, and eventually, a descent into unmanageable debt.

Forgone Wealth Accumulation

By being locked out of homeownership, young people are also locked out of the primary method of wealth accumulation for the middle class: home equity. Instead of paying down a mortgage and building an asset, they are paying rent that builds a landlord’s wealth. This prevents the accumulation of a financial safety net, making them perpetually one or two missed paychecks away from insolvency.

The Evolution of Consumer Credit

The way young people access credit has changed, and with it, the nature of debt. The proliferation of “buy now, pay later” (BNPL) services, high-limit credit cards targeted at students, and the normalization of using debt for everyday expenses have created a precarity that was less common in past generations.

The Fragmentation of Debt

Where previous generations might have had one credit card and a car loan, today’s young adults often have multiple credit cards, several BNPL accounts (each for a small purchase like clothing or electronics), student loans, and perhaps a personal loan. This fragmentation makes it difficult to track total debt exposure. A missed payment on a small BNPL account can trigger late fees and credit score drops that then increase interest rates on other accounts, creating a domino effect.

High-Interest Traps

Many young people, often with limited credit history, fall into the subprime lending market. Credit cards with interest rates above 25% and personal loans with triple-digit APRs are common. What begins as a manageable debt to cover an emergency quickly snowballs as interest accrues faster than payments can be made. For a growing number, filing for bankruptcy becomes the only viable way to stop the compounding interest and predatory collection practices.

Psychological and Social Factors

Beyond the structural economic reasons, there are significant psychological and social factors driving this trend. The way young people perceive and interact with money has been shaped by a lifetime of economic precarity and digital financial management.

The “Financial Nihilism” Phenomenon

A cultural undercurrent among some young people is a sense of “financial nihilism”—the belief that systemic factors make long-term financial stability impossible, so there is little point in trying to save. This can lead to a willingness to incur debt for experiences or goods, with the unspoken expectation that bankruptcy may be an eventual tool to reset. While this is not the primary driver, it normalizes the idea of bankruptcy not as a last resort but as a strategic, if bleak, option.

Shame and Delayed Action

Conversely, many young people delay seeking help due to shame and the stigma associated with financial failure. They may hide mounting debt from family and partners, attempting to manage it alone. By the time they seek advice from a bankruptcy attorney, the situation has often progressed from a manageable problem to a total crisis. The rise of online communities where young people anonymously share their debt struggles is helping to break this stigma, but for many, the shame still leads to destructive delay.

Systemic Gaps in Financial Literacy

A recurring theme in the analysis of why more young people are filing for bankruptcy is a profound lack of accessible, practical financial education. While many high schools offer economics courses, they rarely teach the practical skills of budgeting, understanding compound interest, navigating credit scores, or distinguishing between good and bad debt.

Education Versus Reality

Young people are often taught to view debt as a tool—necessary for college, a car, or a first home. They are rarely taught how to manage the complex interplay of multiple debt accounts, how to prioritize payments during a cash flow crisis, or how to recognize the early warning signs of insolvency. This knowledge gap leaves them vulnerable to predatory lenders and unable to make informed decisions when financial pressure mounts.

The Role of Family Support

The financial safety net provided by family has become increasingly unequal. Young people from affluent families can rely on help with rent, car payments, or a down payment on a home. For those without this support, a single financial shock can be catastrophic. This growing wealth divide means that young people from lower and middle-income backgrounds are disproportionately represented in bankruptcy filings, as they lack the intergenerational wealth transfer that cushions their peers.

The Ripple Effects of Global Uncertainty

The global context of 2026 cannot be ignored. Geopolitical tensions, supply chain disruptions, and the accelerating climate crisis contribute to an overarching sense of instability that impacts employment and costs.

Industry Volatility

Sectors that have historically employed large numbers of young people—technology, retail, hospitality—have experienced significant volatility. Mass layoffs in the tech sector, which many young professionals entered with high hopes and correspondingly high debt loads, have left thousands scrambling. A layoff in a volatile sector often means a prolonged period of unemployment or underemployment, draining savings and forcing reliance on credit cards to cover basic living expenses.

Climate and Insurance Costs

The increasing frequency of climate-related disasters has driven up insurance costs for renters and homeowners, as well as creating direct financial losses. For young people in areas prone to wildfires, floods, or hurricanes, the cost of insuring their possessions and vehicles has skyrocketed. Those without adequate insurance who lose a car or belongings in a disaster may face thousands in unplanned replacement costs, a debt burden that can push them over the edge.

A Closer Look at the Legal and Filing Trends

To fully grasp the scope of the issue, it is important to understand how bankruptcy filings among the young are actually manifesting in 2026.

Chapter 7 Versus Chapter 13

The majority of young filers are opting for Chapter 7 bankruptcy, which allows for the liquidation of unsecured debts (like credit cards and medical bills) and offers a relatively quick discharge, typically within months. This is appealing to young people who have few assets to protect. In contrast, Chapter 13, which involves a repayment plan over three to five years, is more common among those with significant assets or stable income who wish to catch up on secured debts like mortgages. The prevalence of Chapter 7 filings among young people underscores the lack of assets and the urgency to escape crushing unsecured debt.

The Demographic Shift

Data from court filings indicates a significant demographic shift. While bankruptcy has historically been associated with middle-aged individuals, the proportion of filers under 35 has been steadily climbing. This is not merely a function of population size but a true increase in the rate of insolvency among the young. It signals a fundamental shift in which generation is bearing the brunt of the modern economic structure.

Looking Forward: Potential Pathways to Stability

While the picture painted is undoubtedly grim, acknowledging these trends is the first step toward meaningful change. Both policy interventions and individual strategies are emerging to address the crisis.

Policy and Structural Reforms

On the policy front, there is growing discussion around comprehensive student loan reform, including making discharge in bankruptcy easier. There are also calls for expanding affordable healthcare access, implementing rent control measures in high-cost areas, and strengthening safety net programs. The role of financial education in schools is being reevaluated, with some states now mandating personal finance courses for graduation. For those navigating the complex world of business and personal finance, staying informed through reliable resources is crucial. For a foundational understanding of the economic forces at play, exploring resources like What Is Business? can provide context on how broader market trends directly impact individual financial health.

Practical Steps for Individuals

On an individual level, financial advisors stress the importance of proactive debt management. This includes:

- Building an Emergency Fund: Even a small fund of $1,000 can prevent a car repair from becoming a credit card debt spiral.

- Seeking Non-Profit Credit Counseling: Before considering bankruptcy, accredited counselors can help negotiate with creditors and set up manageable repayment plans.

- Understanding Legal Options: Consulting with a bankruptcy attorney is a step many delay too long. An attorney can clarify whether bankruptcy is the right choice or if alternatives like debt settlement or consolidation are viable. For a deeper understanding of the legal framework and historical context of such financial protections, one might consult resources like Wikipedia’s page on Bankruptcy in the United States , which offers a comprehensive overview of the laws governing this process.

The Role of Community and Open Dialogue

Perhaps one of the most powerful shifts is the breaking of silence around financial struggle. Online communities, podcasts, and support groups where young people openly discuss their debt, budgeting failures, and recovery journeys are reducing shame and fostering collective learning. This openness allows individuals to seek help earlier and share strategies for navigating the system.

For those looking to build a more resilient financial future, especially entrepreneurs and young professionals, understanding market dynamics is key. Gaining insights from top business articles and startup tips can empower individuals to create multiple income streams and make informed decisions that protect against the kinds of financial shocks that lead to bankruptcy.

Conclusion

The reasons more young people are filing for bankruptcy in 2026 are a mosaic of systemic failures, economic shifts, and individual vulnerabilities colliding in a perfect storm. It is a story of a generation that did everything it was told—pursued higher education, worked hard, and tried to build a life—only to find that the structural supports that once made such efforts viable have crumbled. The convergence of unaffordable housing, crippling student debt, a volatile job market, and a healthcare system that treats illness as a financial catastrophe has created an environment where insolvency is not a mark of personal failure but often the inevitable outcome of systemic pressures.

As we move forward, addressing this crisis requires a dual approach: systemic changes that make the economy work for young people again, and a cultural shift that empowers individuals with the knowledge and tools to navigate these treacherous financial waters without shame. The high rate of bankruptcy among the young is a warning light on the dashboard of our economy, signaling that for a growing segment of the population, the promise of financial stability is broken. Only by understanding and acting on these root causes can we hope to rebuild a system where young adults can build, rather than merely survive.